Budgeting sounds simple until real life shows up: bills change, income fluctuates, family needs pop up, and you’re supposed to save, invest, and still enjoy life. That’s why people fall into two common traps:

- They pick a budgeting method that’s too strict, feel “bad” when they can’t follow it perfectly, and quit.

- They pick a method that’s too loose, feel “confused” because money disappears, and quit.

The best budget is not the one that looks most impressive. It’s the one you can follow consistently, that helps you spend with intention, and that moves you toward your goals without making you miserable.

Two of the most popular methods are:

- The 50/30/20 Rule (simple percentage-based budgeting)

- Zero-Based Budgeting (detailed, decision-based budgeting where every dollar has a job)

Both can work. Both can fail. And the “winner” depends on your personality, income type, debt level, and how much control you need.

This guide compares them deeply, with practical examples, templates, and decision rules so you can choose the smarter money method for your life.

What Budgeting Is Really For (And Why Most People Do It Wrong)

A budget isn’t a punishment. It’s not a restriction designed to make you feel guilty. A good budget does three things:

- Stops money leaks (small recurring expenses and impulse spending that quietly drain you)

- Creates predictability (you know what you can spend without fear)

- Builds progress (debt payoff, emergency fund, investing, and future goals)

When budgets fail, it’s usually not because the person is “bad with money.” It’s because:

- The method doesn’t match their reality (variable income, family costs, debt, medical expenses)

- The categories are unclear or unrealistic

- They track too much and burn out—or track too little and stay confused

- They don’t plan for irregular expenses (car repairs, gifts, annual fees)

- They expect perfection instead of building a system that survives real life

With that in mind, let’s define the two methods clearly.

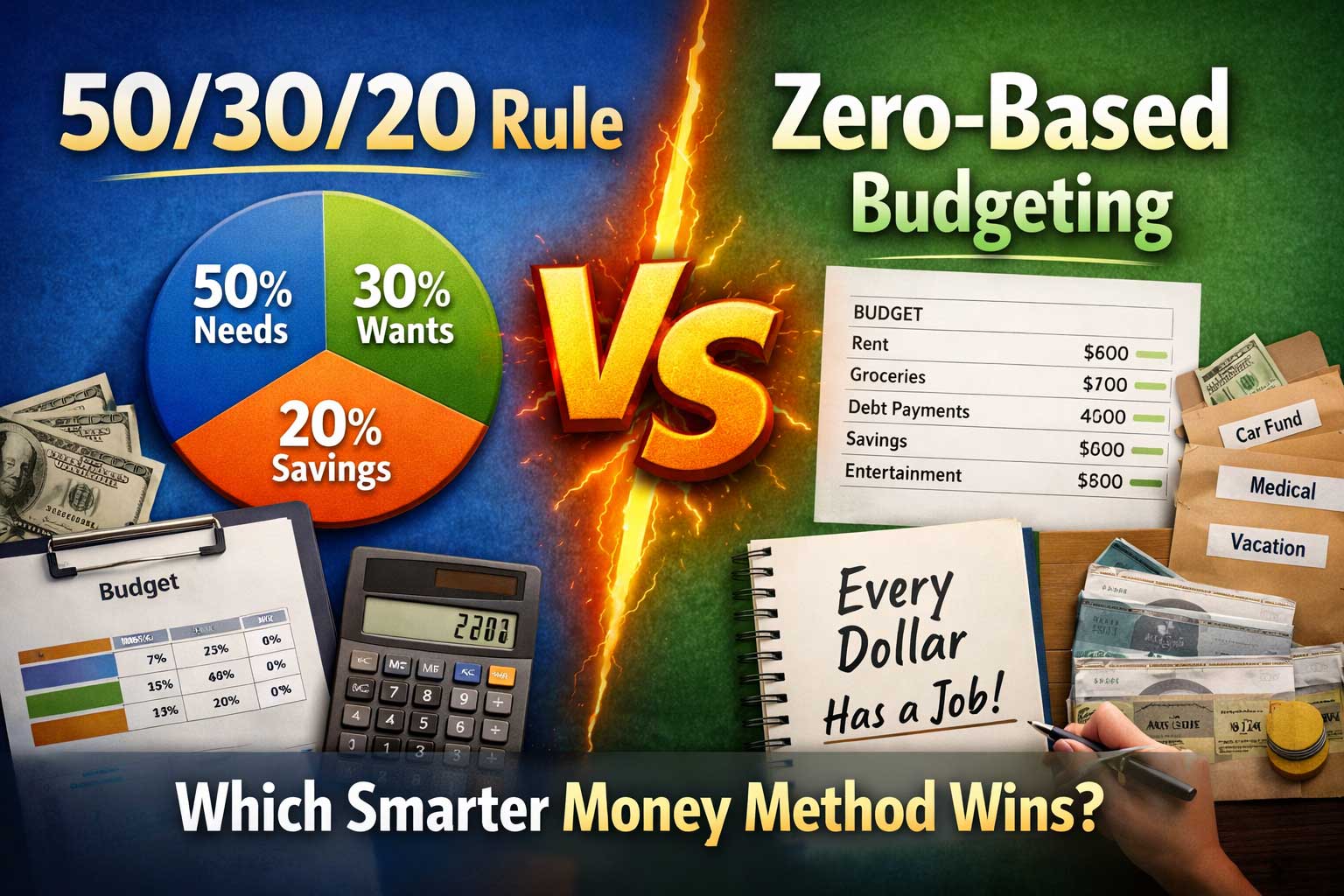

The 50/30/20 Rule Explained (Simple Percent Budgeting)

What it is

The 50/30/20 Rule divides your after-tax income into three buckets:

- 50% Needs: essentials like housing, utilities, groceries, transportation, insurance, minimum debt payments

- 30% Wants: non-essentials like dining out, entertainment, hobbies, subscriptions, travel, upgrades

- 20% Savings & Debt Paydown: emergency fund, retirement investing, extra debt payments beyond minimums

Why it became popular

Because it’s easy. You don’t need 25 categories. You don’t need to track every receipt. You just need to keep your spending in reasonable ranges.

The hidden truth

50/30/20 is not a strict rule of nature. It’s a starting framework—especially useful for people who:

- are new to budgeting

- have stable income

- want a simple system

- don’t have high-interest debt emergencies

- need guidance without complexity

A quick example

If you earn $3,000/month after tax, the guideline becomes:

- Needs: $1,500

- Wants: $900

- Savings/Debt: $600

You then try to keep your monthly spending roughly within those limits.

Zero-Based Budgeting Explained (Every Dollar Gets a Job)

What it is

Zero-based budgeting means you assign every dollar of income to a category until:

Income – Planned Spending – Planned Saving – Planned Debt Payments = 0

That doesn’t mean you end with zero money in your bank account. It means there are zero unassigned dollars.

Every dollar has a purpose: rent, food, sinking funds, investing, giving, fun, future goals. You decide in advance where it goes.

Why it’s powerful

It forces clarity. If you ever wonder “Where did my money go?” this method answers it—because your money goes where you told it to go.

Zero-based budgeting is especially helpful when:

- income is tight

- you’re paying off debt aggressively

- you have irregular income

- you want strong control and fast progress

- you struggle with impulse spending and need guardrails

A simple example

You earn $3,000/month after tax. You build categories like:

- Rent: $1,200

- Utilities: $150

- Groceries: $350

- Transportation: $200

- Insurance: $150

- Minimum debt payments: $250

- Extra debt payment: $200

- Emergency fund: $150

- Investing: $150

- Sinking fund (car repairs): $75

- Sinking fund (gifts): $50

- Eating out: $100

- Entertainment: $75

- Misc: $50

Now every dollar has a job. You’re not guessing.

The Core Difference: Guidance vs Control

Here’s the simplest way to understand it:

- 50/30/20 is a map: it gives you general direction.

- Zero-based budgeting is a GPS: it tells you exactly where every dollar should go.

If you need simplicity and freedom, 50/30/20 feels better.

If you need precision and power, zero-based wins.

But “winning” depends on your situation. So let’s compare them across the things that matter most.

Side-by-Side Comparison: Strengths, Weaknesses, and Best Use Cases

1) Ease of Use (Winner: 50/30/20)

50/30/20 is quick to set up and easy to remember. You can start today without building 30 categories.

Zero-based takes more setup time. You must list categories, amounts, and adjust them as life changes.

Reality check:

If you hate tracking and want a “good enough” plan, 50/30/20 is more likely to be followed.

2) Precision and Control (Winner: Zero-Based)

Zero-based is unbeatable for control. You decide where money goes, and you can spot problems immediately.

50/30/20 can hide leaks because you’re not always tracking detailed spending.

Reality check:

If money tends to “disappear,” zero-based budgeting will reveal where it’s going and help you fix it fast.

3) Debt Payoff Speed (Winner: Zero-Based)

50/30/20 includes debt payoff in the 20% bucket, but it doesn’t guarantee you’re making the right tradeoffs.

Zero-based budgeting can prioritize debt aggressively by intentionally shrinking categories and assigning extra payments.

Reality check:

If you have high-interest debt, you need a method that forces focused decisions. Zero-based usually wins.

4) Lifestyle Balance and Sustainability (Depends)

50/30/20 often feels more livable because it explicitly includes wants (30%). People stick to it because they don’t feel deprived.

Zero-based can feel strict if you make it strict. But it doesn’t have to be. You can budget fun intentionally.

Reality check:

If you’ve quit budgets before because they felt joyless, 50/30/20 may help you stay consistent—or use zero-based with a “fun fund” category built in.

5) Handling Irregular Expenses (Winner: Zero-Based)

Unexpected expenses aren’t unexpected—they’re just irregular. Car repairs, annual subscriptions, birthdays, school fees, medical costs.

Zero-based budgeting shines because it encourages sinking funds (small monthly amounts set aside for upcoming irregular costs).

50/30/20 can handle this too, but many people don’t create the structure, so irregular costs blow up the plan.

6) Handling Variable Income (Winner: Zero-Based, with a simple twist)

If your income changes month to month, percentages can become confusing. Some months you can’t hit 20% savings. Some months you can.

Zero-based budgeting works best when you build it around a baseline income (your lowest expected month) and treat extra income as a separate plan (debt payoff, investing, sinking funds).

A Smarter Comparison Table (Practical, Not Theoretical)

| Factor | 50/30/20 Rule | Zero-Based Budget |

|---|---|---|

| Best for beginners | Excellent | Good but more effort |

| Best for debt payoff | Moderate | Excellent |

| Best for variable income | Moderate | Excellent |

| Tracking effort | Low to medium | Medium to high |

| Helps stop overspending | Medium | High |

| Handles irregular expenses | Medium | High |

| Encourages intentionality | Medium | Very high |

| Sustainability | High for many | High if designed well |

| Setup time | Fast | Slower |

| “Where did my money go?” problem | Sometimes | Rare |

Who Wins for Your Situation? (Real-Life Scenarios)

Scenario A: Stable income, low debt, wants simplicity

You earn a consistent salary. Your bills are predictable. You don’t have crushing debt. Your goal is to save and invest steadily without micromanaging.

Winner: 50/30/20

Why: You benefit from a simple structure that keeps you in healthy ranges.

Scenario B: You feel broke even with decent income

You earn enough, but you don’t know where it goes. Your account drains faster than expected, and you’re not making progress.

Winner: Zero-based

Why: You need visibility, category control, and clear limits.

Scenario C: You have credit card debt and want it gone fast

High-interest debt requires focus. A loose plan can lead to slow payoff and repeated setbacks.

Winner: Zero-based

Why: You can assign extra payments intentionally and cut spending with purpose.

Scenario D: Your “needs” are more than 50%

Many people live in high-cost areas where rent and essentials take more than 50%. Or they have family obligations and necessary expenses above that guideline.

Winner: Zero-based (or a modified percentage plan)

Why: You need a plan built around your reality, not a generic benchmark.

Scenario E: You budget perfectly… then one surprise destroys it

This happens when you don’t plan for irregular expenses.

Winner: Zero-based

Why: Sinking funds prevent “emergency” spending that isn’t truly an emergency.

The Most Important Detail People Miss: Needs vs Wants Isn’t Always Clear

50/30/20 sounds clean, but life is messy:

- Is internet a need? Usually yes (work, school).

- Is a car a need? Depends on location.

- Is a higher phone plan a need? Maybe for work.

- Is therapy a need? Often yes, even if it’s not “required.”

- Is healthy food a need if it costs more? It can be.

Zero-based budgeting handles this better because it doesn’t depend on perfect definitions. You choose categories that match your values and obligations.

That said, 50/30/20 can still work if you treat it as flexible guidelines, not strict labels.

How to Do the 50/30/20 Rule the Smart Way (Step-by-Step)

Step 1: Calculate your true monthly after-tax income

Use the amount that actually hits your bank account, including consistent side income.

If your income varies, use your 3–6 month average or your lowest reliable month.

Step 2: Calculate your essential “Needs”

List your essentials:

- Housing (rent/mortgage)

- Utilities

- Groceries (basic, not luxury)

- Transportation

- Insurance

- Minimum debt payments

- Childcare (if required for work)

- Medical essentials

If your needs are over 50%, don’t panic. It means your reality needs a customized plan.

Step 3: Set a realistic Wants cap

Your wants aren’t the enemy. They’re part of sustainability.

But the goal is to make wants intentional, not automatic.

Step 4: Make the 20% bucket automatic

The easiest way to succeed with 50/30/20 is to automate the “20”:

- auto-transfer to savings

- auto-investing contributions

- automatic extra debt payment

If you wait to “save what’s left,” you usually save nothing.

Step 5: Review monthly, not daily

The strength of 50/30/20 is that it doesn’t require constant attention.

Do a monthly check:

- Are needs creeping up?

- Are wants quietly becoming needs?

- Is the 20% bucket actually happening?

How to Do Zero-Based Budgeting the Smart Way (Step-by-Step)

Step 1: Start with income (and be conservative)

Use your expected after-tax income.

If variable, use a baseline you can count on.

Step 2: List fixed expenses first

These are non-negotiable:

- housing

- insurance

- minimum debt payments

- required transportation

- basic utilities

Step 3: Add variable essentials

- groceries

- fuel/transport

- household supplies

Step 4: Add sinking funds (this is the secret weapon)

Create categories for irregular expenses:

- car repairs

- medical

- gifts

- annual fees

- travel (if important to you)

- home maintenance

- school expenses

Even $20–$50 per category can prevent chaos later.

Step 5: Add goals (debt payoff, savings, investing)

Decide what matters this month.

If debt is urgent, prioritize extra payments.

If stability is urgent, prioritize emergency savings.

Step 6: Add fun on purpose

Zero-based budgeting fails when it becomes emotionally unbearable.

Add:

- eating out

- entertainment

- small treats

- personal spending

A budget without joy often leads to rebound spending.

Step 7: Balance to zero

Assign the remaining dollars until you reach zero unassigned money.

Step 8: Track weekly (simple version)

You don’t need to track every penny perfectly. But you should check category balances weekly to avoid surprises.

Example: Same Income, Two Budgets (So You Can See the Difference)

Assume $4,000/month after tax.

50/30/20 version

- Needs (50%): $2,000

- Wants (30%): $1,200

- Savings/Debt (20%): $800

This is easy, but it doesn’t tell you:

- how much for groceries vs transportation

- whether you can afford a vacation

- how to plan for annual insurance payments

Zero-based version (illustrative)

Income: $4,000

- Rent: $1,500

- Utilities: $200

- Groceries: $450

- Transportation: $250

- Insurance: $200

- Minimum debt payments: $250

- Extra debt payment: $300

- Emergency fund: $250

- Investing: $200

- Sinking fund: car repairs: $75

- Sinking fund: gifts: $50

- Sinking fund: annual fees: $50

- Eating out: $150

- Entertainment: $100

- Personal spending: $75

- Misc buffer: $150

Total: $4,000

Now you can clearly see tradeoffs and make adjustments with confidence.

The “Smarter Money” Scorecard (Which Method Wins by Goal)

If your goal is… less stress and quick simplicity

Winner: 50/30/20

Why: fewer moving parts, easier to maintain, less tracking fatigue.

If your goal is… maximum control and fast progress

Winner: Zero-based

Why: intentional assignment and visibility.

If your goal is… getting out of debt

Winner: Zero-based

Why: forces you to decide what you’ll cut and exactly how much extra you’ll pay.

If your goal is… building consistency when you hate budgeting

Winner: 50/30/20 (or a simplified zero-based)

Why: you’re more likely to stick to something you don’t dread.

If your goal is… stopping the “where did my money go?” mystery

Winner: Zero-based

Why: money goes where you assign it.

If your goal is… handling irregular expenses smoothly

Winner: Zero-based

Why: sinking funds turn surprises into planned expenses.

Common Problems and Fixes (For Both Methods)

Problem 1: Needs are way over 50%

This is extremely common, especially with high rent, family obligations, or medical needs.

Fix options:

- Use a modified ratio: 60/20/20 or 70/15/15 temporarily

- Use zero-based budgeting to prioritize essentials and reduce chaos

- Focus first on stabilizing (emergency fund + reducing big fixed costs if possible)

The point isn’t to match a perfect ratio. The point is to regain control and build progress.

Problem 2: You keep overspending on “small stuff”

Coffee, delivery fees, random shopping, subscriptions—these aren’t huge alone, but together they crush progress.

Fix options:

- Put “small stuff” into one category with a clear limit (zero-based)

- Use a weekly spending cap for wants (either method)

- Create a 24-hour pause rule for non-essential purchases

- Keep one “fun” category so you don’t feel deprived

Problem 3: Your budget fails when life gets busy

A budget must survive busy seasons. If it requires constant attention, it collapses.

Fix options:

- Simplify categories (especially in zero-based)

- Automate savings and bills

- Use weekly check-ins instead of daily tracking

- Build a buffer category (“life happens money”)

Problem 4: You save, then emergencies wipe you out

That usually means you don’t have sinking funds or your emergency fund is too small for your reality.

Fix options:

- Build sinking funds for predictable irregular expenses

- Grow emergency savings to match your risk level (job stability, health, dependents)

- Separate “emergency” from “irregular but expected”

The Best Hybrid Approach (Most People Should Combine Them)

Here’s the truth: you don’t have to marry one method forever. You can combine them into a system that’s both simple and powerful.

Hybrid Method: “50/30/20 Guardrails + Zero-Based Details”

- Use 50/30/20 as your big-picture health check

- Use zero-based budgeting for your Needs and Savings/Debt to guarantee progress

- Keep Wants simple with one or two categories to avoid tracking burnout

This hybrid works especially well when you want structure without feeling trapped.

Decision Guide: Choose Your Winner in 60 Seconds

Pick 50/30/20 if most of these are true:

- Your income is stable

- Your expenses are predictable

- You’re not drowning in debt

- You want a simple plan you’ll actually follow

- You prefer flexibility over precision

Pick Zero-Based if most of these are true:

- You feel unsure where your money goes

- You have debt you want to eliminate fast

- Your income varies or you have commission/freelance work

- You need strict clarity and intentional limits

- You want to plan for irregular expenses and big goals

If you’re split, use the hybrid.

How to Make Either Method “Smarter” (Advanced Practical Tips)

1) Use a “Money Ladder” (priority order)

No matter your budgeting style, decide the order your money should serve:

- Essentials (keep life stable)

- Minimum debt payments (protect credit and avoid fees)

- Emergency fund (avoid future debt)

- High-interest debt payoff (fastest guaranteed “return”)

- Investing (long-term growth)

- Lifestyle upgrades (only after progress is consistent)

When you have a priority ladder, budgeting becomes decision-making, not guesswork.

2) Budget by week if you overspend early

Many people blow the month in the first 10 days.

Fix: Convert categories into weekly limits.

Example: $400/month eating out becomes $100/week.

This works in both methods and improves control dramatically.

3) Create a “Sinking Fund Bundle”

Instead of 10 tiny sinking funds, bundle them:

- “Car + Home Maintenance”

- “Gifts + Holidays”

- “Annual Fees”

- “Medical Buffer”

Fewer categories = more consistency.

4) Add a “Good, Better, Best” version of your budget

This is powerful for variable income.

- Good (baseline): covers essentials + minimums

- Better: adds savings and sinking funds

- Best: adds extra debt payoff and investing

Then, when you earn more, you don’t waste it—you already have a plan for it.

5) Track progress with one number

Budgets feel motivating when progress is visible.

Choose one primary metric:

- debt balance going down

- emergency fund going up

- net worth increasing

- investing contributions increasing

A budget that feels rewarding becomes sustainable.

The Verdict: Which Smarter Money Method Wins?

If “winning” means simplicity, fast setup, and lifestyle balance, the 50/30/20 rule often wins—especially for stable incomes and beginner-friendly structure.

If “winning” means control, clarity, and faster goal achievement, zero-based budgeting wins—especially for debt payoff, irregular income, or stopping money leaks.

But the smartest answer is this:

The winning method is the one you can stick with for the next 90 days while making measurable progress.

If you’re overwhelmed, start with 50/30/20 for momentum.

If you’re stressed, confused, or in debt, use zero-based budgeting for control.

If you want the best of both worlds, combine them.

FAQs (For Search Intent and Real-Life Clarity)

Is the 50/30/20 rule realistic if my rent is high?

It can still be useful as a benchmark, but you may need a modified ratio or zero-based budgeting to reflect your reality. High housing costs often require a custom plan.

Does zero-based budgeting mean I can’t have fun?

No. It means fun is planned on purpose. In fact, adding a fun category often prevents binge spending later.

Which method is better for investing?

Both can work. Zero-based helps ensure you consistently invest by assigning a specific amount. 50/30/20 encourages investing in the 20% bucket, but it’s easier to “accidentally skip” unless it’s automated.

What if I’m bad at tracking expenses?

Use a simplified zero-based budget with fewer categories, plus weekly check-ins. Or start with 50/30/20 and automate savings to protect progress.

How long should I test a method before switching?

Give it at least one full month, ideally three months, so you can adjust. Most “failures” are just unrealistic category amounts that need tuning.